Yesterday the

OECD predicted the UK economy would contract in the first quarter of 2012. It led the news for a while (pre-Galloway), vying for contention with pricier pasties and petrol pump panic.

The state of the economy is a vastly more important issue than both of those things, yet the way in which it is reported perhaps explains why people are more interested in pasties - and perhaps why they're right to be.

Firstly, we should define 'recession'. A technical recession is widely agreed to be two consecutive quarters of 'negative growth'.

Negative growth is a ridiculous term: economists' jargon when the English language provides ample alternatives: contraction, shrinkage, reduction. I personally favour 'contraction'.

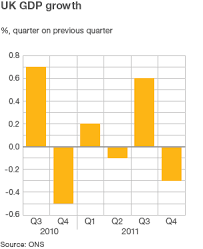

At the end of each quarter (of a year, i.e. three months), the government (and indeed governments around the world) announce the level of economic growth - the change in our gross domestic product (GDP).

GDP is value of all the goods and services produced which includes private and public consumption, government expenditure and investments, as well as exports less imports.

So if there is economic growth then GDP has risen (relative to the last time it was recorded). If GDP has declined, then there is contraction (aka negative growth).

So back to the OECD, which predicted that in the first three months of 2012 the UK economy will have contracted by 0.1% - following a contraction of 0.3% in the last three months of 2011.

Leave aside that many close watchers of UK economic trends think the OECD has got it wrong anyway (especially after the economic boost of all the panic petrol buying), but even if the UK economy has contracted by 0.1%, what does that mean?

Well we know what it means technically: that the value of all the goods and services produced has contracted by 0.1% in the last three months. And if that is for a second consecutive quarter, as would be the case in the UK currently, then it would be a technical recession.

Somewhat illogically the economy is not in recession if it contracts by 2% in one quarter, grows by 0.1% the next and then contracts by 1% the one after. Yet two consectutive quarters of 0.1% contraction are a 'recession', even though the former case is worse.

So it's clear to me we should change our definition of recession to something that more accurately tells us the state of the economy: so how about a technical recession being redefined as contraction over an annual basis. In other words, if we look at the average of the last four quarters (or year, as most people know it).

But what does any of this mean to anyone personally or - to be less individualistic - to a community or to the economy?

Is growth that relevant? What does Mr Wilson or Ms Patel do when they hear the economy has contracted by 0.6%? A: About the same as they do when they hear the FTSE has dropped 1%. Fuck all, because it doesn't really much matter (and there's not much they can do about it).

What matters to people is their own living standards, the inequality in their community, the level of unemployment. And surely we (as fellow socialist readers of this blog) want an economy and economic measures that treat people as paramount.

So here's what's important: how does the change in your income relate to the change in inflation? That matters whether you're in waged work or receiving out of work benefits. It measures whether your living standards have risen or fallen.

Or what about the gap between rich and poor? Numerous researchers including Wilkinson & Pickett and Danny Dorling have shown the damaging effects of inequality on life chances through a variety of metrics.

And then there's unemployment - undoubtedly bad because of what it means for the individuals concerned, and also economically inefficient because it means we are paying for talent to be left idle (receiving benefits) instead of enabling that person to contribute to the economy (pay taxes).

So instead of measuring badly what matters less, why not prioritise measuring what matters most:

- Living standards

- Inequality

- Unemployment

Because next month (on 25 April), despite the OECD's prediction, I suspect that the news will be reporting that the economy has returned to growth (probably only 0.1-0.4%) and Osborne will be welcoming it as a new dawn and an endorsement of austerity - only for the economy to contract in the second quarter.

This obsession with growth encourages politicians (as those from all parties did) to ignore rising inequality and do nothing about unsustainable debt-fuelled growth.

As Ann Pettifor said on Newsnight (watch online) (discussing the OECD prediction) the government should have used the budget "to spend on infrastructure, which would create jobs to create the income to pay back the debts".

That way, we'd reduce unemployment, increase living standards, reduce inequality and, also, generate stable economic growth.

The reality is that Osborne's austerity policies mean rising unemployment, falling living standards for most, and rising inequality. Bad for people and bad for the economy.

If we, as the left, want a new economy then we should be emphasising new ways of measuring its performance too.

Are the austerians right and the opponents of austerity proved wrong? Is Osborne's strategy vindicated?

Are the austerians right and the opponents of austerity proved wrong? Is Osborne's strategy vindicated?